December 2021 Outlook — Inflation, Inflation, Inflation

Image by Farshad Rezvanian

Forecast Quick Notes

· Strengthening dollar helps improve my outlook of emerging markets and global real estate

· Inflation in Europe counteracts the stronger dollar and keeps my outlook flat

· Rising yield spreads cool my outlook on US real estate

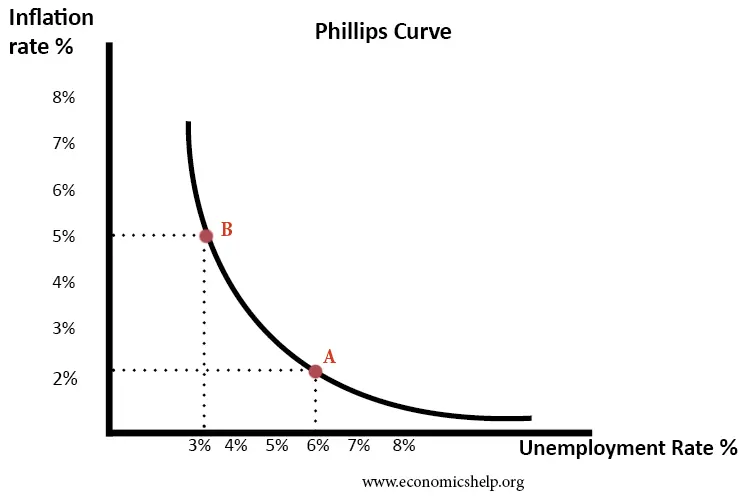

Happy December! 2021 is coming to a close, and hopefully more people will be able to spend time with their loved ones than last year. Before recapping market performance in November for the asset classes I follow, I want to discuss the Phillips Curve. The Phillips Curve is a theoretical relationship between inflation and unemployment. The theory behind the curve is that inflation is caused by economic growth and thus leads to a lower unemployment rate. See the image below from Economics Help 2.

The numbers in the chart are purely for illustration – an unemployment rate of 6% is not always tied to an inflation rate of 2%. The main takeaway is that higher inflation is correlated with lower unemployment. Since its introduction, it has been shown to not always hold. Stagflation seen in the 1970s, where inflation rose along with unemployment, was a real-life counterexample to the Phillips Curve. Since as far back as the 1960s, economists have argued the Curve is only applicable in the short-run3. Nevertheless, it remains a useful lens to analyze inflation and unemployment. Viewing some charts from the Federal Reserve in St. Louis, one can see that from 2012 to 2020, the Phillips Curve failed to hold. Unemployment slowly but consistently fell, and inflation trended sideways.

Unemployment over Time

Inflation over Time

After the recession in 2020 (shaded period in the above charts), however, the Phillips Curve appears to have come back with a vengeance. Inflation has marched from a trough of nearly 0% to just above 6% while unemployment peaked at about 15% and has since fallen to a little over 4%. In other words, inflation has risen as unemployment has fallen. A logical question to ask is what changed before and after this most recent recession. It’s neither possible to identify every contributor to inflation nor say exactly how much each source is contributing. A strong economy is likely part of the reason for inflation, and supply chain issues may be another. The potential reason I want to zoom in on is wage growth.

Wage Growth over Time

While wages have been steadily rising with minor setbacks along the way, they’ve rocketed in 2021. Employers likely pass on at least part if not most of these increased costs to consumers. This creates an interesting storm. Causal relationships are difficult to pin down with certainty, so I won’t try to do that. What I’ll say instead is that a falling unemployment rate, a tight labor market, and rising prices are moving together. There’s a limit to how high prices can go in the short-run, and the same is true for wages. Unemployment can only theoretically hit zero before either the labor force or labor participation rate or both must increase. When this cycle slows or stops, it’s hard to say where the economy will land. The Federal Reserve has a dual mandate to keep unemployment low and inflation under control. How and if this will be accomplished is yet to be seen.

Switching gears to market performance in November, the S&P 500 was down about 75 basis points while its growth and value counterparts were up 1.5% and down 3.2% respectively. While inflation remains elevated, fears of inflation fell somewhat in November. One of the ways to combat inflation is to increase interest rates, and rising rates tend to favor value stocks more than growth stocks. If inflation doesn’t need to be countered, there’s less of a reason to raise rates; the market in aggregate may have determined that keeping rates steady was the more likely scenario than increasing rates and tilted towards growth stocks. Jerome Powell’s recent comments about tapering bond purchases earlier than expected have turned this notion on its head, but I’ll discuss that with the forecasts.

Internationally, the MSCI Emerging Markets Index fell 4% while the MSCI EAFE Index fell 4.5%. In both asset classes, the performance of the US dollar acted as a headwind. With the US dollar strengthening, the returns of companies in international markets fell in dollar-terms. Inflation rose in Europe, and although it isn’t as high as it is in the US, this likely led to some negative sentiment towards stocks in the EAFE region. Performance of Chinese technology companies contributed to the decline in emerging market equities broadly.

US real estate fell about 2.2%. This is likely due to decreased or at least decelerating demand for housing. New housing starts were down, and high yield interest rate spreads rose. Higher interest rates make borrowing more difficult for consumers, and this may have led to a slight cooling off in demand. Global real estate fell about 3.7%. Part of this decline was likely due to the strengthening of the dollar. Finally, US core fixed income rose about 10 basis points.

Jumping to the present, a lot has happened very recently. In the final week of November, a new variant of the COVID-19 virus called the omicron variant was reported in South Africa. Since then, cases have been detected in other countries, including the United States. While little is certain about this variant, it seems to currently be more resistant to the vaccines than previous variants. The world will know more as more data is available, but the uncertainty around the new variant could be part of the reason the end of November and start of December have been difficult for risky assets broadly. Within the US, the notion of inflation being transitory is starting to be challenged. As reported on CNBC, Jerome Powell has signaled that the tapering (slowing or reduction) of bond purchases may occur earlier than the Federal Reserve has previously suggested1. Inflation has arrived faster and with more intensity than the Fed had previously forecast which is what’s driving the conversation around a faster taper. The potential for higher interest rates along with some technology companies issuing weaker guidance than expected have played a part in sharp price drops in certain technology stocks. US growth stocks haven’t been hit so hard as a whole, but it’s possible that they could follow. While I had anticipated some increase in volatility in US stocks (See my November Outlook), I can honestly say I didn’t expect this much volatility.

Looking to the future, my US equity forecasts remain mostly flat from last month. I expect growth to very modestly outperform value and for US equities broadly to generate low single-digit returns. Given my prior statement that higher interest rates tend to favor value stocks, one might wonder why I still favor growth. The exact relationship between higher interest rates and the return of growth and value stocks isn’t perfectly linear. My view is that the effect of rates on growth and value stocks is more step-like; certain rate-level thresholds need to be breached before the impacts derail growth trajectories. I also focus on other factors for these asset classes, and my algorithm currently assigns a higher degree of importance to these other factors relative to interest rates. I don’t ignore interest rates entirely, but until they take on greater importance in my framework or my other factors shift dramatically, I’ll likely continue to favor growth over value.

The biggest changes in my outlook from last month pertain to emerging market equities and international real estate. Mainly due to the strengthening and accelerating performance of the US dollar, my forecasts for both of these asset classes have risen. While I’m still bearish on global real estate, I’m significantly less bearish. For emerging market equities, I’ve gone from being slightly bearish to slightly bullish. One other factor potentially playing a favorable role in my emerging markets forecast is risk appetite; when risk appetite is low or falling, forward returns in the past have been better for emerging market equities. Although a strengthening dollar should likely also favor international developed equities, this was countered by the rise of inflation in Europe, so my forecast for international developed equities was mostly unchanged from last month.

The rise in high yield spreads reduced my US real estate forecast. Borrowing becomes less attractive as interest rates rise, so demand tends to fall. I still think returns will be positive, but I’m not as confident as I was a month ago.

Lastly, my US core fixed income forecast is flat. Rising yields would reduce the present value of cash flows for existing bonds but would lead to higher coupon payments for future bonds. For now, I’m viewing that effect as a wash. My US core fixed income forecast and US core equity forecast are still quite close to one another, so I wouldn’t be surprised to see continued volatility over the next few months.

That’s all I have for this piece. Only time will tell if volatility seen in the US technology sector will meaningfully spread to other sectors and regions of the market. Until next time, happy holidays and happy investing.

2. https://www.economicshelp.org/blog/1364/economics/phillips-curve-explained/